Over recent months, I’ve made no secret of my view that the energy market is in need of serious reform.

I’m pleased to see that my comments have helped spark a lot of discussion – this is an area where national debate is desperately needed.

In saying that, we need the debate to be an informed one, so it’s concerning that the commentary from those seeking to maintain the status quo has often omitted or twisted the facts.

Here are three points we need to be really clear on.

First, energy prices are unaffordable, and the problems started well before last year’s crisis.

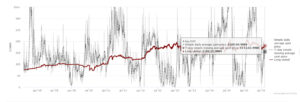

The chart below tracks prices on the forward electricity contracts market, which dictates the cost of supply contracts. As you can see, prices have roughly doubled over the last five-six years, from around $90 MWh in 2019 to $180 MWh today. For many commercial energy users, the spike in prices last year was a case of the straw breaking the camel’s back.

While plenty of other countries are also grappling with energy affordability challenges, that doesn’t make our situation acceptable.

New Zealand’s forward prices are significantly above the cost of new generation (in an efficient market, the two should remain close) and much higher than those in Australia –more than double those on Victoria’s forward market, for instance.

High forward prices tell us that the market expects generation of electricity to remain expensive, and the security levels risky, for some time to come.

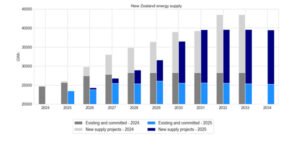

Second, while new generation is happening, it’s not happening at the scale or pace required.

Much has been made of the gentailers’ pipeline of investment, but it hasn’t translated into the abundance of new projects that is needed. Since 2020, 1.2GW of new generation has been built, and a further 1GW of construction has been committed to (versus planned) over the coming years.

This leaves us well short of the target that the gentailers themselves have identified of 4.8GW of new generation for the current decade. Critically, that target doesn’t factor in the rapid decline in gas, which necessitates an even greater increase in capacity.

Much more generation will be needed to meet projected demand, and more still if New Zealand hopes to make the most of big data, AI and the higher productivity and standards of living that would come from these technology enablers.

Expectations about new generation coming to market have plummeted between last year and this year. Transpower’s 2025 Security of Supply Assessment shows that anticipated new supply for the 2026 year fell by 70-80%, despite extremely high wholesale prices in the near-term (which should help incentivise new generation).

Third, the market is hyper concentrated, choking off competition.

Underlying supply and affordability issues is the fact that the market is starved of competition. The gentailers control 92% of generation and around 87% of retail and, as I’ve argued before, market domination combined with vertical integration provides gentailers with the incentive – and the power – to hold back supply and foreclose competition.

New entrants are being shut out of the market by the lack of availability of long-term contracts, and lack of access to firming.

Over the past year, the trend has been towards even greater concentration, with Contact’s acquisition of Manawa, Meridian’s purchase of NZ Wind farms, Genesis’ acquisition of Helios sites, and the collapse of Prime Energy.

This is why reform needs to be bold, and needs to start now.